YOU TAKE CARE OF EVERYONE.

BUT WHO TAKES CARE OF YOU?

Here's How You'll Be Helping Your Grandkids:

We do. We sweat the details and free up your time:

#1: Tax Strategy

Why throw money out the window? Taxes only going up.

#2: Delegate

Save time: delegate all the detail and coordination to us.

#3: Individualized

We do not believe "one size fits all." You get tailored advice.

#4: Asset Protection

At a certain level of wealth, it is critical to protect your assets.

#5: Invest with Purpose

Our clients prefer a dual focus: invest for profit and purpose.

#6: Modern Investing

Not just stocks|bonds, but gold, crypto and real estate as well.

#7: Private Deal Flow

Often, the best deals are invitation only.

#8: Dedicated Team

You get an assigned point person focusing on you.

Our clients are business owners,

CEOs, C-suite execs and entrepreneurs.

And none of them have a minute to spare.

Which is why they value our investment

expertise and the time we save them.

Who doesn't want more time for family, golf or travel?

LET'S TALK INVESTMENTS

The stock market is volatile.

To help offset that volatility, we find and screen private investments to complement your stock portfolio. These are often invite-only and often cannot be accessed by investors directly. The best of these can generate meaningful returns and increase diversification.

Example private investments:

Real estate collateralized loan fund (no debt at Fund-level, monthly cash distributions, max 70% loan to value); historically has yielded 7-8% per year and distributes cash on a monthly basis

Distressed investment fund: produces better than average returns during period of change and distress; targets 20%+ annualized returns) -- 5 year hold

DIP lending fund: targets 15% annualized return -- 3 year hold; fully collateralized loans

An Israeli biotech company that is radically reducing re-incision risk with initial focus on breast cancer survivors, and next use cases targeting liver and lungs (3-10x target return, 5 years)

P.S. Don't Underestimate The Stock Market

While the market will continue to be volatile, forward-looking sectors tend to generate measurable wealth and we believe the next decade will be no exception. Given the massive wave of change being fueled by technology, the key is to pick the right sectors and active management.

Top 5 Investing Mistakes We See

Sitting on cash OR investing in near-zero return bonds and getting hosed by inflation

Letting emotions get the better of you and either being under-invested or over-invested at the wrong time and then either needlessly locking in a loss or missing a lot of upside (sitting in cash)

Failing to do in-depth due diligence and getting trapped in unprofitable private deals

Paying unnecessary taxes when you could be using that cash to fund your retirement bucket (especially true for business owners who can take advantage of legal IRS approved methods)

Not letting your winners run and failing to cut your losers short to protect your capital

Financial Planning

Get Answers to Your Questions

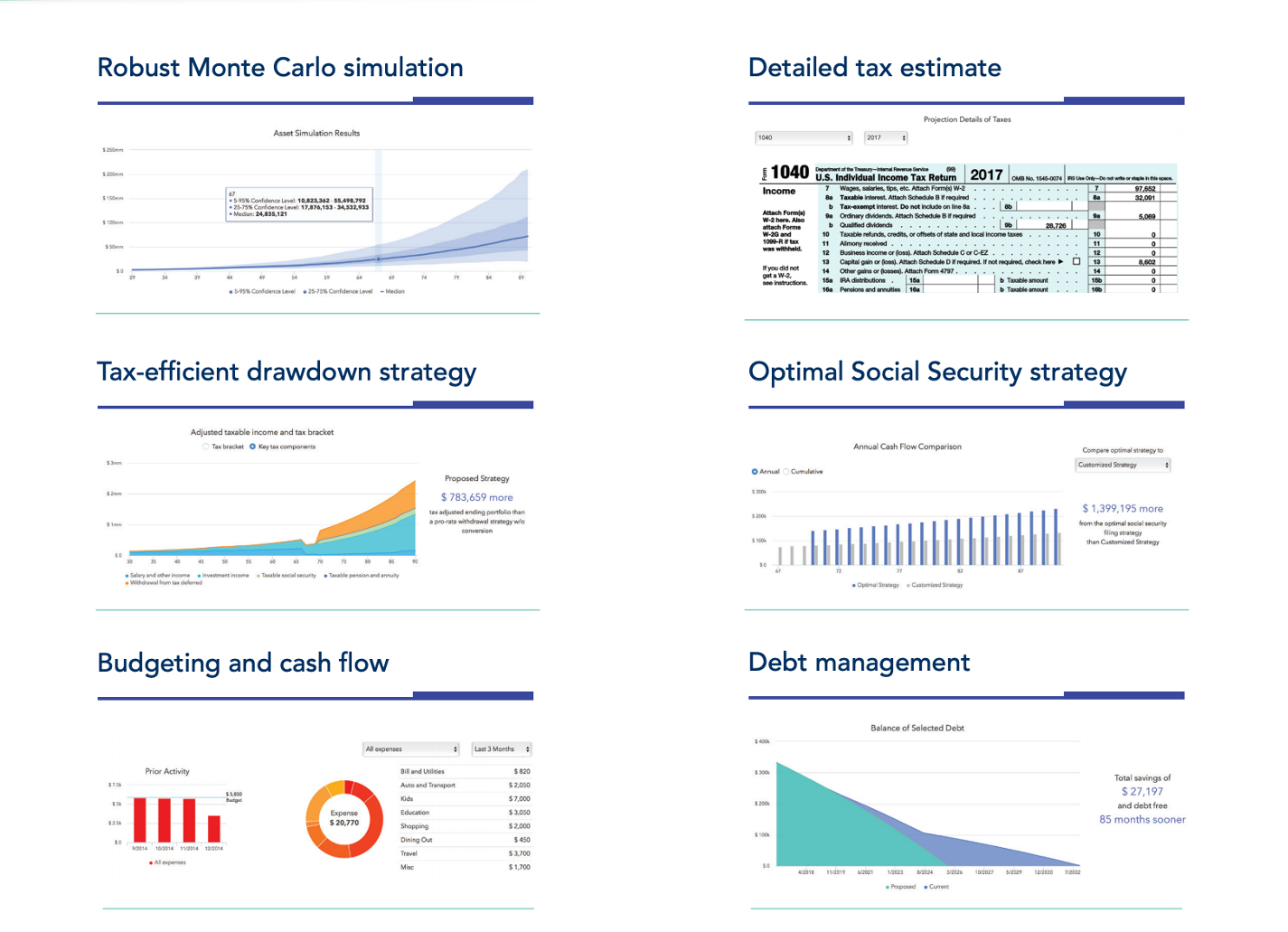

Questions like: 'How much would I need to sell my company for, to never worry about money again?', 'What is the best way to give to our children?', 'How can we pay less in taxes as a business owner?', 'How can we protect our assets?' and others. Below you can see some of the tools we use to refine and quantify the answers to your questions.

Based in Austin, Texas

Serving Clients Coast to Coast

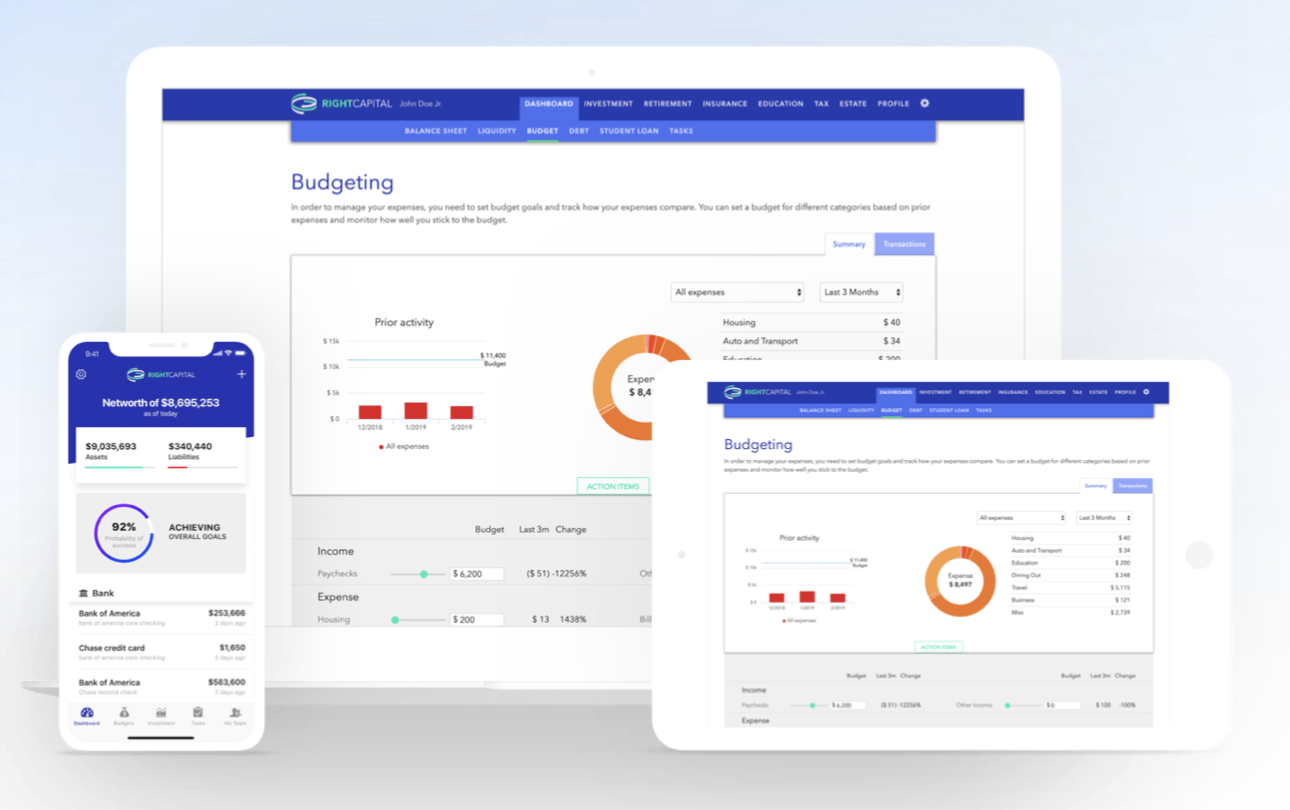

100% Tech-Enabled and Clients Coast to Coast

Clients today expect

state of the art technology.

And that's what you get.

All digital. 24/7 access.

We give you an app you can use on your

phone or tablet to see your whole picture.

We organize and store your key estate docs

online; there when you need them and easy to

share with others as you see fit. No paper!

The Platinum Plan:

1. Year 1: $800 upfront

2. Year 2: $25/month

- Includes Initial Plan (2 hours)

- 60 min per year in consultation or coaching

- usable anytime but time does not "rollover"

- month to month after the first year

- plan benefit is the sheer affordability

The Platinum Plan:

Here's a Clip @ Our Firm and Co-Founder, Stefan Whitwell

Need a better tax plan?

World-Class Custodian

TIME LEFT IN 2026

I know what you're thinking:

"this can wait..." But what if?

What if U.S. federal income tax rates go up? Many business leaders feel this is inevitable, just a matter of when, especially given the non-stop level of government spending.

What if Congress slashes the estate tax exemption before you can move a meaningful chunk of your wealth out of your estate? Would you be ok with the I.R.S. getting as much as your kids?

What if you were so busy during the sale of your business that you missed out on some tax planning techniques that can't be done after the sale -- resulting in your overpaying millions in taxes?

What if the stock market suffered a pull back: are you positioned to take advantage of that if we see one this year? Or would that be stressful given how your assets are currently positioned?

Remember: "Fortune Favors the Prepared."

With one call, you can have a team that will save you time, watch your investments like a hawk and look for ways to reduce your tax bill.

The Platinum Plan:

The Platinum Plan: